EMEA mobile device market continues upward trend in Q2

Posted on 21-Jul-2004 08:02

| Filed under: News

: Mobile

Research firm Canalys sees good growth across handheld, wireless handheld and smart phone segments.

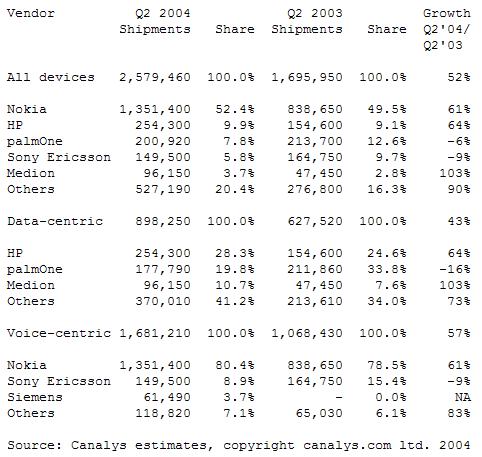

Overall EMEA mobile device market in Q2 2004 up 52% on Q2 2003

Data-centric (handhelds, wireless handhelds) up 43%; voice-centric (smart/feature phones) up 57%

"Converged" devices up 63%, but standalone handheld shipments also up a respectable 31%

Nokia leads in voice-centric devices and in overall market, increases share slightly

HP leads from palmOne in data-centric segment, for fourth quarter in succession

For Canalys, following last quarter's lull in GPS navigation bundle activity, Q2 saw the standalone handheld market boosted by retail success for several vendors, including Medion, Mio Technology and Yakumo. Combined with the gains made by vendors such as HP, Acer and FSC, the market for handhelds in EMEA grew 31% year-on-year, despite shipment falls for palmOne, Toshiba, NEC CI and the exit of ViewSonic. Wireless handhelds grew at an even higher rate (200%), with RIM (up 230%), T-Mobile (up 154%) and O2 (up 79%) helping to raise the total data-centric segment up 43% year-on-year to just under 900,000 units, its third highest quarter in the past four and a half years.

"This demonstrates that there is still significant potential in the handheld market in EMEA, despite the negative news coming from other worldwide regions," said Chris Jones, Canalys director and senior analyst. "But clearly not everyone is benefiting in the same way. The less well-known brands, through highly competitive navigation bundles, are taking significant share through retail, while major IT brands, for example Dell and Toshiba, are having little impact."

Jones expects that more vendors will look at the high growth in the wireless handheld segment and be tempted to play in this space, but warns against coming in unprepared. "IT vendors have tried before and met with little success. They should not underestimate the challenge of building relationships with enough operators in enough countries to make the venture worthwhile. Having a good product that appeals to the design sensibilities and meets the functional requirements of EMEA customers is the first step. But it is only really the operators themselves and RIM, which has adopted a very operator-centric channel approach, who have had any kind of success in this segment."

From an OS perspective, Symbian continues to rule the voice-centric mobile device segment, with 94% market share. Microsoft's share fell back to around 4% after a relatively good Q1, while PalmSource's, through the Treo 600, increased to just under 2%. Although the prospect of Nokia dominating the Symbian consortium in shareholding terms has diminished, it still represented 85% of all Symbian devices shipped in Q2, up from 81% in Q1.

"Nokia is still the only vendor with a wide, segmented and frequently refreshed range of Symbian devices," said analyst Rachel Lashford. "Sony Ericsson has demonstrated its willingness and ability to respond to user feedback and provide incremental improvements to its smart phone, but it is still only really offering one product. The other licensees are in a similar situation and they are all unlikely to make up much ground on Nokia until their ranges expand."