Bevan Muollo, a senior construction manager, bought a house in Wellington in 2021 for $1.2 million. Five years later, he’s selling it at a loss of $300,000.

Muollo is among 5000 Kiwis who bought in the housing market boom and subsequently sold at a gross loss. That’s about 60% of people who bought in that period.

Property analyst Cotality defines the latest peak as the last three months of 2021 and first three of 2022.

An estimated 5000 people who bought homes over that period have since sold for a lower price, said its chief economist, Kelvin Davidson.

“That’s about 60% of all purchasers in that window who have subsequently resold at a gross loss.”

says the media network that was promoting buying up large at the peak.

no sympathy here for those who over extended themselves chasing the pot of gold. however it does suck for those fhbers who where tricked into overpaying by the mass media who was "helping fhbers" until the profit for the sellers disappeared.

that article is really just a "talk up the market" piece.

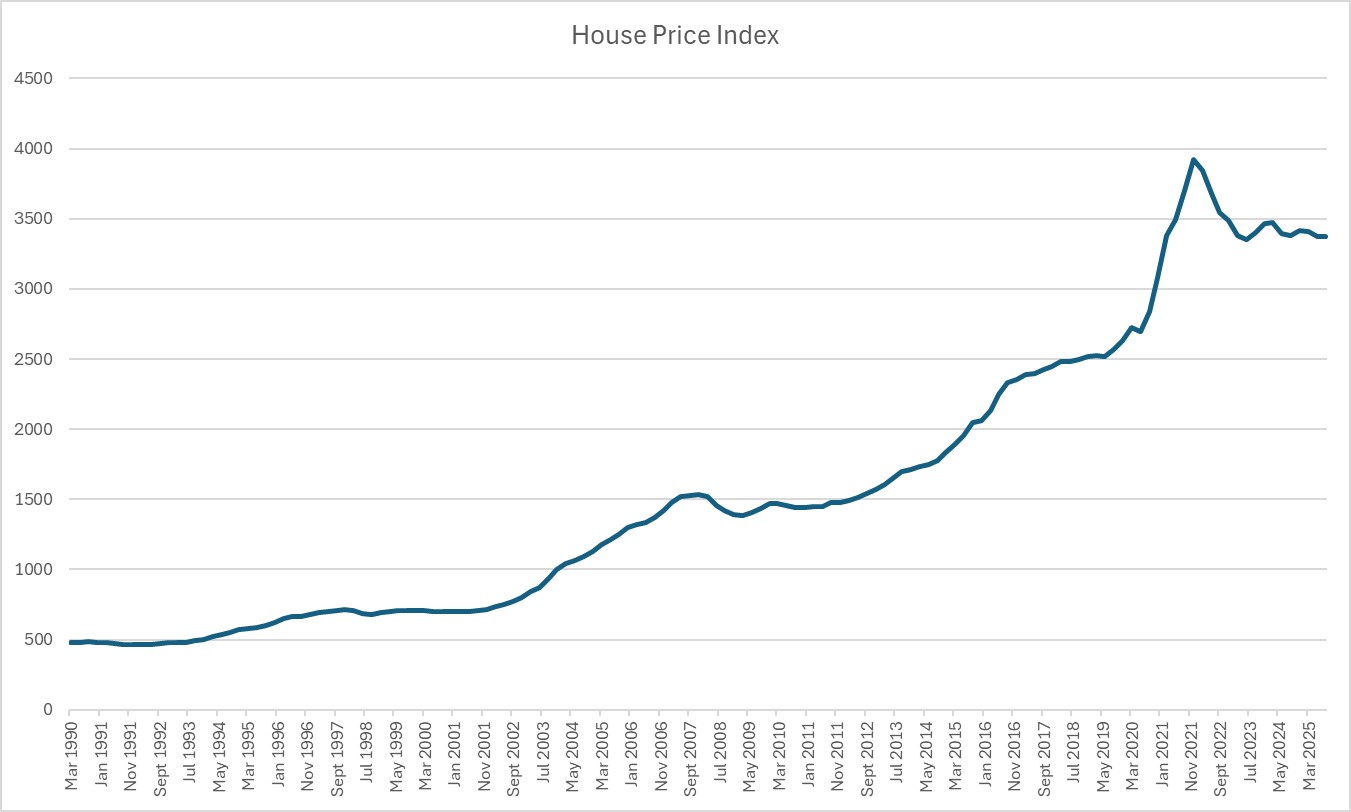

To be fair, if it was smoothed out from 2001 it would look fairly consistent.

I honestly don't know what the answer is short of firm DTI ratios. And applying it savagely across investors too.

there is a graph around that shows more of a wider veiw. basically prices falling until mid 70's, then steadily increasing pretty much a constant rate. a few dips eg gfc, but it bounces back up and continues on at similar rate. theres a bounce up with covid and down again after.

the problem at the moment is its running into natural ceilings. eg people don't have enough lifespan to spread a mortgage across, but that hasn't stopped people pushing for longer mortgages and even generational mortgages. businesses can't afford to increase wages so home owners can give it all away to the sellers and banks. plus food is more important than housing. even the housing shrinkflation thats going on can't change those factors. its rather bad that they are pushing shrinkflation onto new homes. price doesn't go up but what you get is just worse.

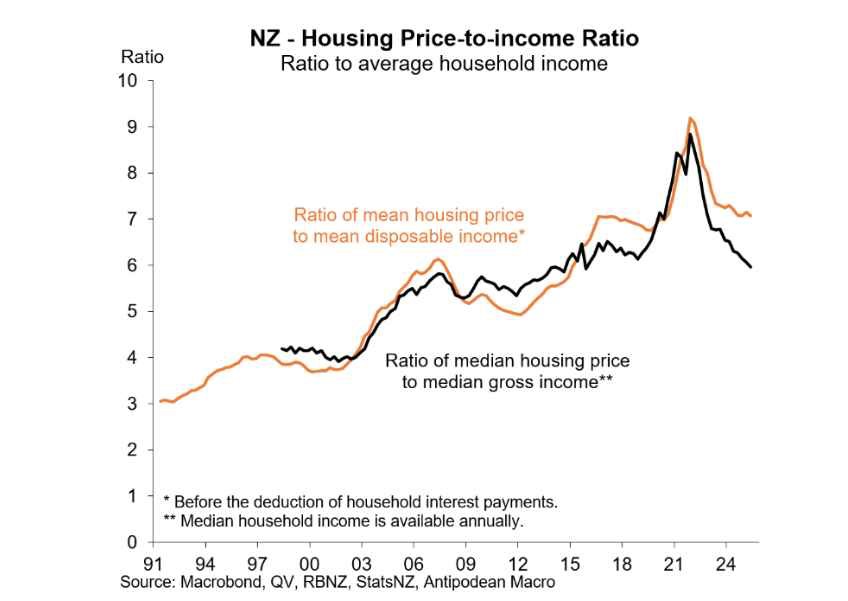

Although Incomes and general prices have also risen since 1990...

A better metric is probably house price to income... which shows the price level is around 1/2 as affordable as it was in the 1990s...

But well down from the COVID lunacy...

Has household always been the metric? As in two incomes? I wonder say in the eighties when my parent's bought their first it was on one income.

its median income. no mention of how many income earners per house. tho today a minimum of two is almost always required. also not sure if its simply median value of all income or just those that own houses.

one of the problems here is there is a ton of different ways to measure and compare, usually depending on what outcome you want to show. the devil is in the detail. eg notice the median disposable income graph which is before removing interest payments, but is it before removing principle payments?

one of the problems here is there is a ton of different ways to measure and compare, usually depending on what outcome you want to show. the devil is in the detail. eg notice the median disposable income graph which is before removing interest payments, but is it before removing principle payments?

I genuinely don't think it's that complicated. I think it's is simply average disposable income. IE whatever you have left after expenses excluding the mortgage.

one of the problems here is there is a ton of different ways to measure and compare, usually depending on what outcome you want to show. the devil is in the detail. eg notice the median disposable income graph which is before removing interest payments, but is it before removing principle payments?

I genuinely don't think it's that complicated. I think it's is simply average disposable income. IE whatever you have left after expenses excluding the mortgage.

Edit, it's not that either.

It's just gross income to house price as a ratio.

black line is ratio of gross income to housing. ie what people are spending on housing. other line is disposable income to housing. if you take interest out of it, then it shows what effect interest rates have. if you take cost of housing and interest rates out of it, it shows what you can spend on housing after the bills are paid.

The thing is that NZ has had a house price crash, but the NZ media are very reluctant to state that fact. pretty much everyone who has said, or is saying House prices were recovering over the last 3 years have some form of vested interest in the housing market. Taking into account inflation, House prices are dropping. I was a FHB that purchased during COVID so its value is a lot less if I sold. People say you can buy and sell in the same market so it isn’t going to affect you, but they don’t factor in that you may also lose your deposit if the house is worth less than the amount you borrowed, making it not possible to buy another unless you have that money for a deposit. Australia’s house prices have continued to increase since Covid and they haven’t had the same housing crash

The thing is that NZ has had a house price crash, but the NZ media are very reluctant to state that fact. pretty much everyone who has said, or is saying House prices were recovering over the last 3 years have some form of vested interest in the housing market. Taking into account inflation, House prices are dropping. I was a FHB that purchased during COVID so its value is a lot less if I sold. People say you can buy and sell in the same market so it isn’t going to affect you, but they don’t factor in that you may also lose your deposit if the house is worth less than the amount you borrowed, making it not possible to buy another unless you have that money for a deposit. Australia’s house prices have continued to increase since Covid and they haven’t had the same housing crash

i think Liam Dann (herald) did a story on it some time ago. but most media has vested interest due to RE market advertising. people even got suckered with the "increase in fhber's", framing data to pretend fhbers are out buying in huge numbers so get in quick before its all gone.

the thing is, if you didn't over extended yourself then its typically a matter of just wait. you took on the debt, you pay it off. life is not risk free, its up to the person to take on as much risk as they like.

kiwis have poured insane amounts into housing and its biting nz in the rear. but no one wants to fix that. even the failing construction sector has no interesting in making a stable housing market so they have a stable construction industry. they prefer chasing gold and failing companies. its crazy. everyone wants to make a quick buck and flip nz the bird.

I was a FHB that purchased during COVID so its value is a lot less if I sold. People say you can buy and sell in the same market so it isn’t going to affect you, but they don’t factor in that you may also lose your deposit if the house is worth less than the amount you borrowed, making it not possible to buy another unless you have that money for a deposit.

Yes if you're in negative equity the only thing you can do is sit tight. Not the worst option, but assuming no redundancy of course.

black line is ratio of gross income to housing. ie what people are spending on housing. other line is disposable income to housing. if you take interest out of it, then it shows what effect interest rates have. if you take cost of housing and interest rates out of it, it shows what you can spend on housing after the bills are paid.

I don't think it needs to be overthought. Obviously we are all aware the lower a DTI ratio the better. Most people should be doing their maths on about 8% interest rates anyway.

If you have two people earning $200K then a mortgage of $1M is doable on one of those salaries at 8%.

Going down, $150k would service $600k comfortably at 8%

I don't think it needs to be overthought. Obviously we are all aware the lower a DTI ratio the better. Most people should be doing their maths on about 8% interest rates anyway.

If you have two people earning $200K then a mortgage of $1M is doable on one of those salaries at 8%.

Going down, $150k would service $600k comfortably at 8%

the problem is $600k is now an entry level house and median income is ~$70k. so it takes 2x people both on median income. so yes, 150k can service it at 8% but thats entry level house, not average house. average fhber is ~40 years old, almost at peak income and income will be declining for half the loan. loose your job at 55 and it can be a real struggle to get another due to agism, and you still have half the mortgage to go.

Are you subscribed to our RSS feed? You can download the latest headlines and summaries from our stories directly

to your computer or smartphone by using a feed reader.