If it’s means tested including assets, then I’ll be better off selling assets and give up savings and spend all money above the amount.

Some people spend all money as soon as get, others go without and put aside for better life latter.

So if worked entire life, paid over a 1/3 or more of income in tax including GST, then expected to receive nothing in retirement vs someone that has not worked or save, yeah right.

on that note, make it universal income and then you don't need super.

yes, but then young people also get it. Maybe better to make the first 20k of earnings tax free.

above a certain age everyone gets it and if your working you pay it back through taxes. the big advantage is its automatic welfare with virtually no admin cost. i really detest the whole "take the benefit off them to force them to work" idea, its low hanging fruit. you just end up making more crims. the govt making people reapply for benefits twice as often is a very expensive screw you to poor people. spending your tax dollars for no gain. having recently been made redundant and gone through all that, its not nice or helpful.

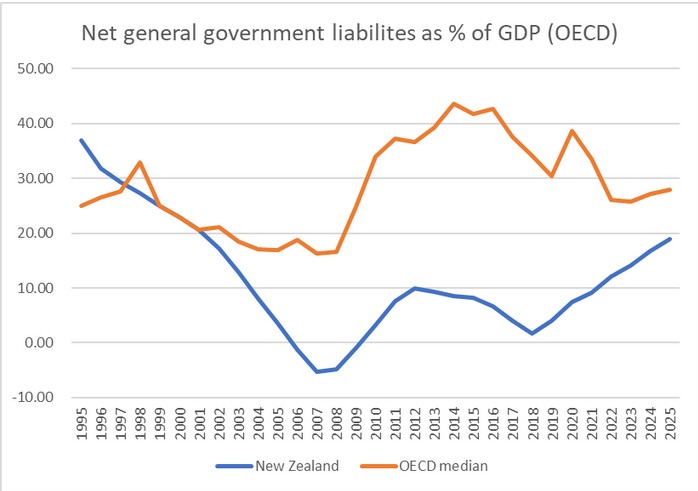

Which is what the Cullen fund was supposed to address. No one has really bagged National for stopping paying into it when they were previously in. There was a bull market where it would now be worth a lot more than it is currently. Also remember Key saying that NZ could afford to continue having the super entitlement age set to 65 and didn’t need it increasing. Then as soon as he resigns National increased it to 67 for most under 50, but it got reversed back to 65 when Labour got back in. But NZers see it as an entitlement, not a benefit. Overseas countries do look at NZ super with envy and it is simple. Nationals changes to KiwiSaver over the years has also cost NZers a lot in lost retirement savings.

people think its an entitlement because they mistakenly thing they have always being paying into it.

nz super is nice and simple, its just a terrible way to fund it. one day kiwisaver will be around long enough and compulsory, then super will be done away with.

New Zealand super is an entitlement. The jobseeker benefit is an entitlement. Working for families is an entitlement. If you meet the qualifications for these forms of welfare you are entitled to receive them.

An entitlement doesn’t mean that the qualification criteria for the entitlement or the value paid can’t change. It just means if you meet the criteria that you are entitled to receive the welfare payment. People use entitlement instead of welfare or benefit because it makes them feel better about receiving welfare, not because it has any meaning more than a benefit.

Which is what the Cullen fund was supposed to address. No one has really bagged National for stopping paying into it when they were previously in. There was a bull market where it would now be worth a lot more than it is currently. Also remember Key saying that NZ could afford to continue having the super entitlement age set to 65 and didn’t need it increasing. Then as soon as he resigns National increased it to 67 for most under 50, but it got reversed back to 65 when Labour got back in. But NZers see it as an entitlement, not a benefit. Overseas countries do look at NZ super with envy and it is simple. Nationals changes to KiwiSaver over the years has also cost NZers a lot in lost retirement savings.

There was probably a bit more to the decision to suspend the payments, the country was coming out of the GFC and any payments to Super Fund would have had to come from borrowings. The reduction in net debt gave the next Government room to work with.

Which is what the Cullen fund was supposed to address. No one has really bagged National for stopping paying into it when they were previously in. There was a bull market where it would now be worth a lot more than it is currently. Also remember Key saying that NZ could afford to continue having the super entitlement age set to 65 and didn’t need it increasing. Then as soon as he resigns National increased it to 67 for most under 50, but it got reversed back to 65 when Labour got back in. But NZers see it as an entitlement, not a benefit. Overseas countries do look at NZ super with envy and it is simple. Nationals changes to KiwiSaver over the years has also cost NZers a lot in lost retirement savings.

There was probably a bit more to the decision to suspend the payments, the country was coming out of the GFC and any payments to Super Fund would have had to come from borrowings. The reduction in net debt gave the next Government room to work with.

That's not neccesarily true. While they claimed that was the case they also made significant changes to the tax system (reduction in income tax, particularly at the top income level and raising GST) which meant that there was also potentially a significant reduction in government income. Whether you view that as a good decision or not depends on your view around taxation and government provision of services.

What it did do was kick the can further down the road and avoided them being stuck with making difficult decisions.

National also clobbered a 1974 Labour manatory pension contribution scheme.

National has a sound track record of making sure the future of superannuation is an ongoing issue.

It's quite funny how perverse this debate is in New Zealand. New Zealand Superannuation is entirely socialist in nature, despite the jibe earlier in this thread. Individual accounts which paid out an actual pension, based on individual contributions, was characterised as communist.

There’s been a lot of chatter about means testing, raising the age of claim etc.

I was ruminating on it and one thing I’ve not seen suggested is to permit delayed receipt.

For example, each year which you decline to take it once you’re eligible, some sort of bonus occurs.

This could be an increase in what you get once you do claim or a percentage of what you would have received had you claimed it being paid into your Kiwisaver account. EG each year you get, say, 25% of the total Super

that you were technically entitled to paid into your Kiwisaver. This reduces your cost to the taxpayer by 75% each year but provides the individual with a useful incentive.

Sadly it seems this original post was largely overlooked, it probably isn’t workable exactly as described, but deferral is an interesting idea and treasury/actuaries love this sort of calculation. There might be something here which could help a bit I think.

Also putting it into Kiwisaver would be helpful, except it can be withdrawn immediately at 65, would you deny access to this for these years too? (Seems like a good idea)?

In summary - the benefit to you is more benefit in future. Benefit to government is deferred liability plus people dying before deferral reached.

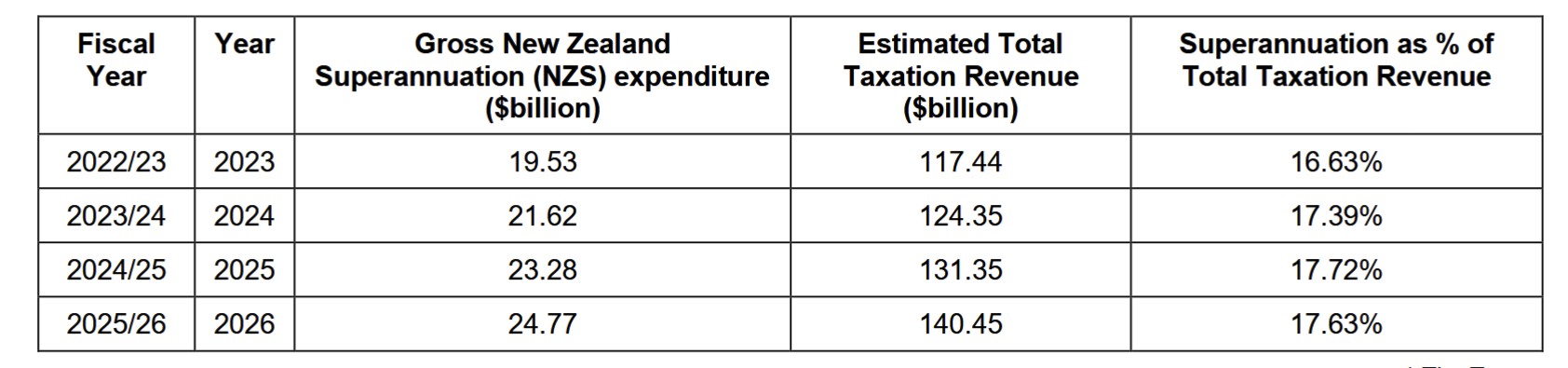

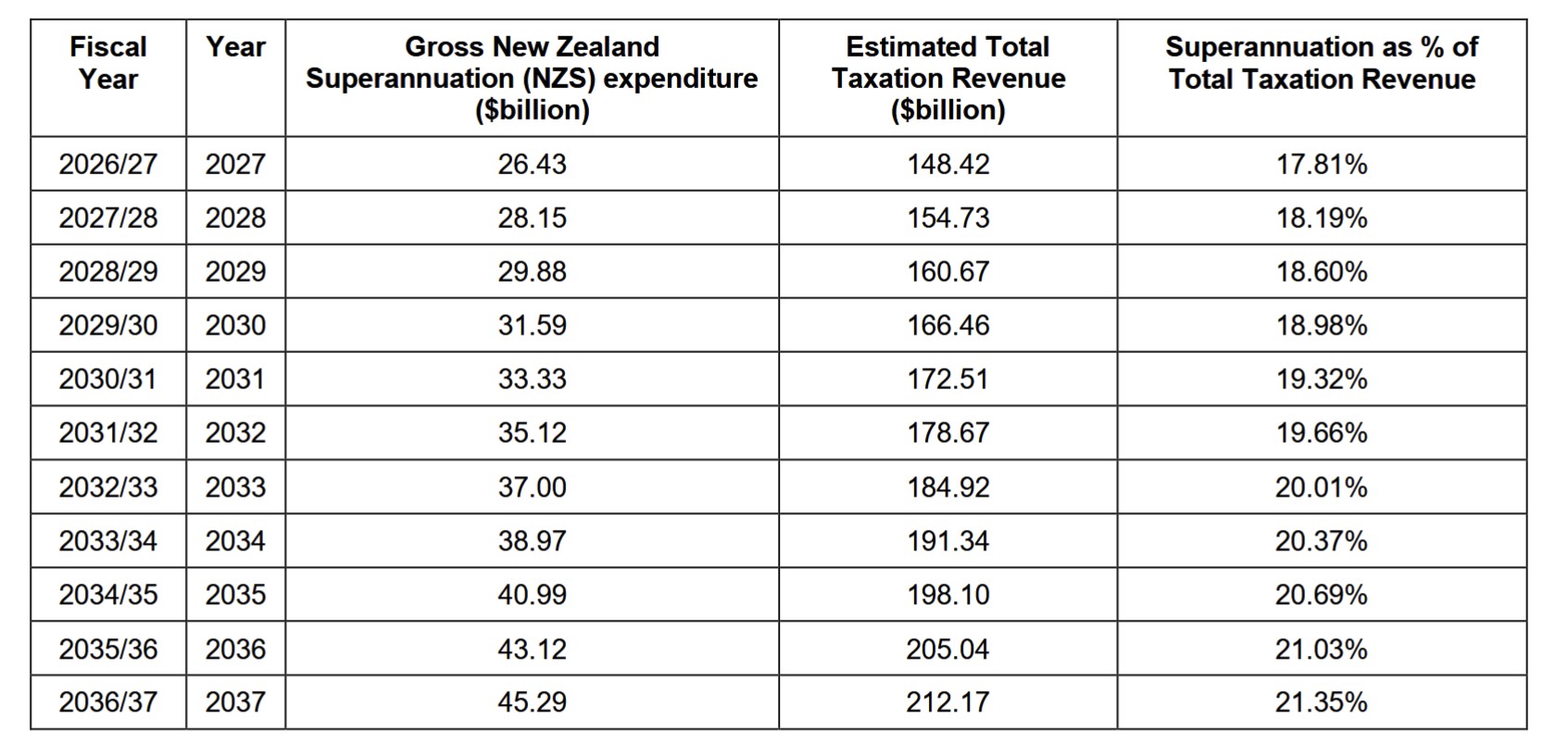

In terms of the rest of the conversation, the other part of the lack of affordability is the likely length of retirement (life span growth) as well as the number of retirees.

I personally would love Treasury to be more open with some of the forecasts and options because it is going to take us being a lot more informed about our choices to make better ones.

I personally would love Treasury to be more open with some of the forecasts and options because it is going to take us being a lot more informed about our choices to make better ones.

Treasury projects out and reports every six months as part of the budget and HYEFU. Most people don’t want to know what the forecasts are showing. This hasn’t been a secret for many years.

Most people don’t want to know what the forecasts are showing. This hasn’t been a secret for many years.

Pretty much this. NZ Super has been a political football for decades.

1) People who currently qualify for NZ Super are a massive voting bloc. 2) People close to NZ Super age don't want to feel like the ladder is pulled up and they 'miss' out. 3) There is an assumption that if you pay taxes, you will be entitled to NZ super.... sorry peeps, this isn't a qualification criteria, it's based on years lived.

To be eligible for New Zealand Superannuation, you generally need to have lived in New Zealand, the Cook Islands, Niue, or Tokelau for a certain number of years after turning 20.

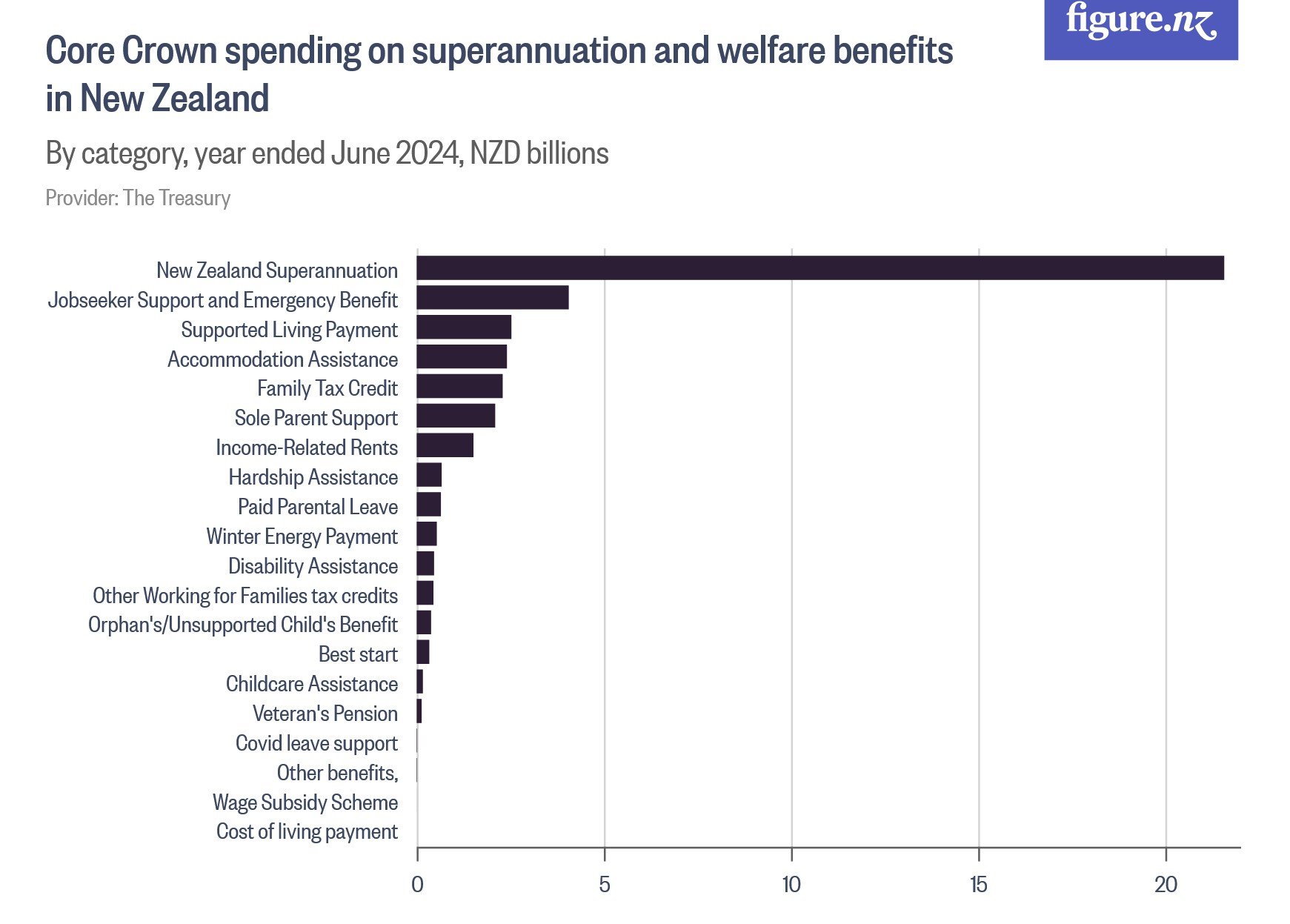

4) There is an assumption of a social contract; the social contract is the government and budget of the day. Parties can and will change it up whenever it is politically viable for them to do so. 5) NZ Super is a benefit, it is social welfare, it is not a pension. In fact, it is the biggest benefit in terms of cost and is about 50% of the total cost of all benefits paid.

7) Our current taxes aren't being saved for our future; current taxes are budgeted and spent now. 8) By the time I get to the current NZ Super age, that ladder is going to be so far up from where it is now... is that "fair"? Only a fool will expect the world to be fair.

There have already been changes to NZ Super Eligibility:

increase in the minimum residency requirement for New Zealand Superannuation (NZ Super) from 10 to 20 years. The residency increase has been described as a way to address the long-term sustainability of the NZ Super scheme. It was introduced by the NZS & Retirement Income (Fair Residency) Amendment Act 2021.

9) I think it is good to have a conversation about NZ Super and what our expectations are as a country. However, I think the conversation should include the entire taxation system because borrowing money for tax cuts and treasury forecasts are showing that we are going to hit a wall.

The UK State Pension age is currently set at 66 for men and women. While you cannot access your pension entitlement before this age, you can delay it until you’re older than 65. If you choose to defer your State Pension you’ll receive a higher income based on the amount you would’ve received, plus interest. Depending on when you’re due to reach State Pension age, delaying claiming State Pension could make you eligible for a lump-sum payment.

The UK State Pension age is currently set at 66 for men and women. While you cannot access your pension entitlement before this age, you can delay it until you’re older than 65. If you choose to defer your State Pension you’ll receive a higher income based on the amount you would’ve received, plus interest. Depending on when you’re due to reach State Pension age, delaying claiming State Pension could make you eligible for a lump-sum payment.

while that sounds like a good idea, its rather pointless. it also doesn't solve the issue because they end up paying the same amount. its just you choose to let the govt borrow money from you.

i think most would take the money before the govt changes the rules again, and go stick it in their kiwisaver/savings fund etc. the end result for you is the same, except your in control of it not the govt.

Some people spend all money as soon as get, others go without and put aside for better life latter.

So if worked entire life, paid over a 1/3 or more of income in tax including GST, then expected to receive nothing in retirement vs someone that has not worked or save, yeah right.

Think of it like this. While you paid income tax and GST, the government spent all the money as soon as they got it. They didn't put some aside for later. There's nothing from your taxes left for you to receive. The only way you will receive something is if future generations continue to agree to keep paying out of their taxes towards your retirement.

Some people spend all money as soon as get, others go without and put aside for better life latter.

So if worked entire life, paid over a 1/3 or more of income in tax including GST, then expected to receive nothing in retirement vs someone that has not worked or save, yeah right.

Think of it like this. While you paid income tax and GST, the government spent all the money as soon as they got it. They didn't put some aside for later. There's nothing from your taxes left for you to receive. The only way you will receive something is if future generations continue to agree to keep paying out of their taxes towards your retirement.

yeah, and some of taxes I’ve paid have gone into paying other peoples retirement, for it not to continue what a have.

Are you subscribed to our RSS feed? You can download the latest headlines and summaries from our stories directly

to your computer or smartphone by using a feed reader.