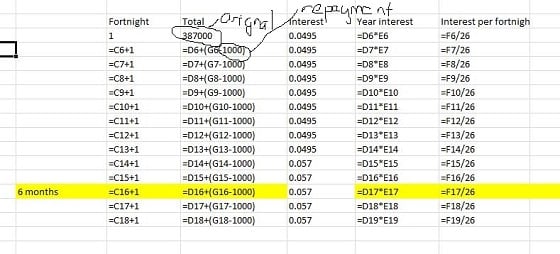

Newbie question on but not for me. I am compiling a spreadsheet like numbers myself ... let's say a fixed interest rate is that calculated monthly? Ie - you take the fixed % for the amount of the loan then per month ... subtract the payments you make and this cycle repeats for the next month?

Cheers